Inverted Duty Structure (IDS) Refunds Under GST 2.0 – A Relief Path for Businesses

Introduction

When GST was first rolled out, it was built on a simple promise: tax should never become a cost to business. The idea was that credit would flow seamlessly through the value chain. But in practice, whenever the tax rate on inputs is higher than the tax rate on outputs, businesses run into what’s called an Inverted Duty Structure (IDS). The result? A pile-up of Input Tax Credit (ITC) that companies can’t easily use.

Section 54(3)(ii) of the CGST Act, 2017 already provides a remedy — refunds of accumulated ITC. But with GST 2.0 coming into effect on 22nd September 2025, rate rationalisations have widened the gap in some sectors. Corrugated box manufacturers, in particular, have been hit hard.

The GST Council and CBIC have now stepped in. From 1st November 2025, 90% of IDS refunds will be released provisionally, giving businesses much-needed liquidity without long waits.

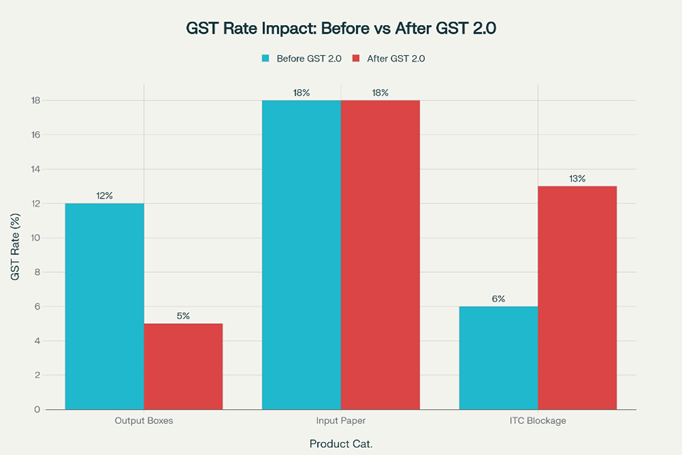

IDS in Action: Corrugated Boxes Post-GST 2.0

- Before 22.09.2025: Corrugated boxes were taxed at 12%, while inputs major kraft paper attracted 12% and other attract 18 %. The mismatch was there, but manageable.

- After 22.09.2025: The output tax on corrugated boxes dropped to just 5%, while inputs increased to 18% form earlier 12 %.

Impact in numbers:

- Buy kraft paper worth ₹1,00,000 → pay ₹18,000 GST.

- Sell finished corrugated boxes worth ₹1,00,000 → output GST liability only ₹5,000.

- That leaves ₹13,000 of blocked ITC per lakh of turnover.

For MSMEs, this kind of working capital blockage is not just inconvenient — it can be crippling. Refunds are the only way to keep cash flows healthy.

Industry’s Long-Standing Plea

The corrugated box industry has been raising this issue for years. As the backbone of India’s packaging ecosystem — serving FMCG, pharma, e-commerce, and exports — it cannot afford liquidity squeezes.

Industry bodies have repeatedly highlighted that:

- Margins are already razor-thin; blocking 13% of turnover in ITC is unsustainable.

- Liquidity stress threatens the survival of smaller players.

- Without timely refunds, competitiveness across supply chains takes a direct hit.

The Eastern India Corrugated Box Manufacturers Association has confirmed that over 20,000 MSMEs are at risk of closure. The industry, which employs over one million people and processes seven million tonnes of kraft paper annually, faces unprecedented liquidity challenges

The government’s decision to release 90% of refunds upfront is therefore not just a policy tweak — it’s a lifeline.

Legal Foundation for IDS Refunds

The right to refunds isn’t a matter of discretion; it’s firmly rooted in law:

- Section 54(3)(ii), CGST Act: Allows refunds where input tax exceeds output tax.

- Rule 89(5), CGST Rules: Prescribes the formula for calculating refunds.

- Supreme Court in CCE vs. Ratan Melting & Wire Industries (2008): Clarified that circulars cannot override statutory provisions — refunds are a vested right.

- CBIC Circular No. 173/05/2022-GST: Confirmed that refunds are admissible even when inputs and outputs are the same goods, provided the lower output rate is due to a concessional notification.

Together, these provisions make it clear: taxpayers facing IDS are entitled to refunds, and no contrary clarification can take that away.

The New Relief: 90% Provisional Refunds (Effective 01.11.2025)

To ease the liquidity crunch, the GST Council has recommended extending provisional refunds (earlier available only for zero-rated supplies) to IDS cases as well.

Here’s how it will work:

- 90% of the refund claim will be sanctioned upfront, provisionally.

- System-driven risk checks will ensure revenue safeguards.

- The remaining 10% will be released after detailed verification.

This strikes a balance — genuine taxpayers get quick relief, while the system still guards against misuse.

Practical Guidance for Businesses

- File on time: Submit claims in Form GST RFD-01 with Rule 89(5) workings, invoices, and stock details.

- Leverage provisional refunds: From November 2025, expect faster inflows of 90% of your claim.

- Keep records clean: Stock ledgers, reconciliations, and accumulation details will be critical.

- Be audit-ready: The final 10% refund will depend on compliance and accurate documentation.

Conclusion

The corrugated box sector is a textbook case of the inverted duty structure problem: inputs taxed at 18%, outputs at 5%, and a huge ITC pile-up. GST 2.0’s rate rationalisation may have triggered the issue, but the law — through Section 54(3)(ii) — provides the solution.

Now, with the added relief of 90% provisional refunds from 1st November 2025, businesses finally have a workable path forward. This dual assurance — statutory entitlement plus immediate liquidity — not only restores GST’s promise of tax neutrality but also strengthens trust in India’s evolving indirect tax regime.

Author’s Note

CA Ketan Agarwal specialising in GST, taxation, and compliance advisory. With experience across practice and industry, he regularly writes on indirect tax reforms and their impact on businesses, with a focus on practical solutions for MSMEs.

Disclaimer: The views expressed are personal and intended for informational purposes only. They do not constitute professional or legal advice.

Ref :-

- https://gstcouncil.gov.in/sites/default/files/2025-09/press_release_press_information_bureau.pdf?utm.

- https://taxinformation.cbic.gov.in/content/html/tax_repository/gst/acts/2017_CGST_act/active/chapter11/section54_v1.00.html

- https://cbic-gst.gov.in/pdf/Circular-173-05-2022-GST.pdf

- GST ‘disparity’ poses threat to survival of corrugated box makers: Industry association

- Some paper products get GST relief, others see a rise

Leave a Reply